The egg processing market is valued at approximately USD 33.3 billion in 2024 and is expected to grow to USD 41.9 billion by 2029, reflecting a compound annual growth rate (CAGR) of 4.7% during this period. Several factors influence the global egg processing market’s development, including shifts in consumer preferences, advances in processing technologies, and evolving food safety regulations. Additionally, population growth, urbanization, and changing dietary habits significantly impact the demand and supply dynamics within this sector.

A notable study published in October 2022 in Frontiers in Animal Science examined consumer perceptions of egg processing across 14 countries, such as Australia, Brazil, China, India, Malaysia, Nigeria, the UK, and the US. Drawing on responses from 4,292 participants, the research revealed detailed insights into consumer attitudes toward egg production systems and hen welfare. An overwhelming 76% of respondents (excluding Nigeria) favored eggs from hens raised in cage-free environments. Furthermore, 72% highlighted the importance of minimizing hen suffering during egg production, underscoring a widespread concern for animal welfare. These insights offer valuable guidance to industry players and animal welfare advocates aiming to align production practices with consumer expectations.

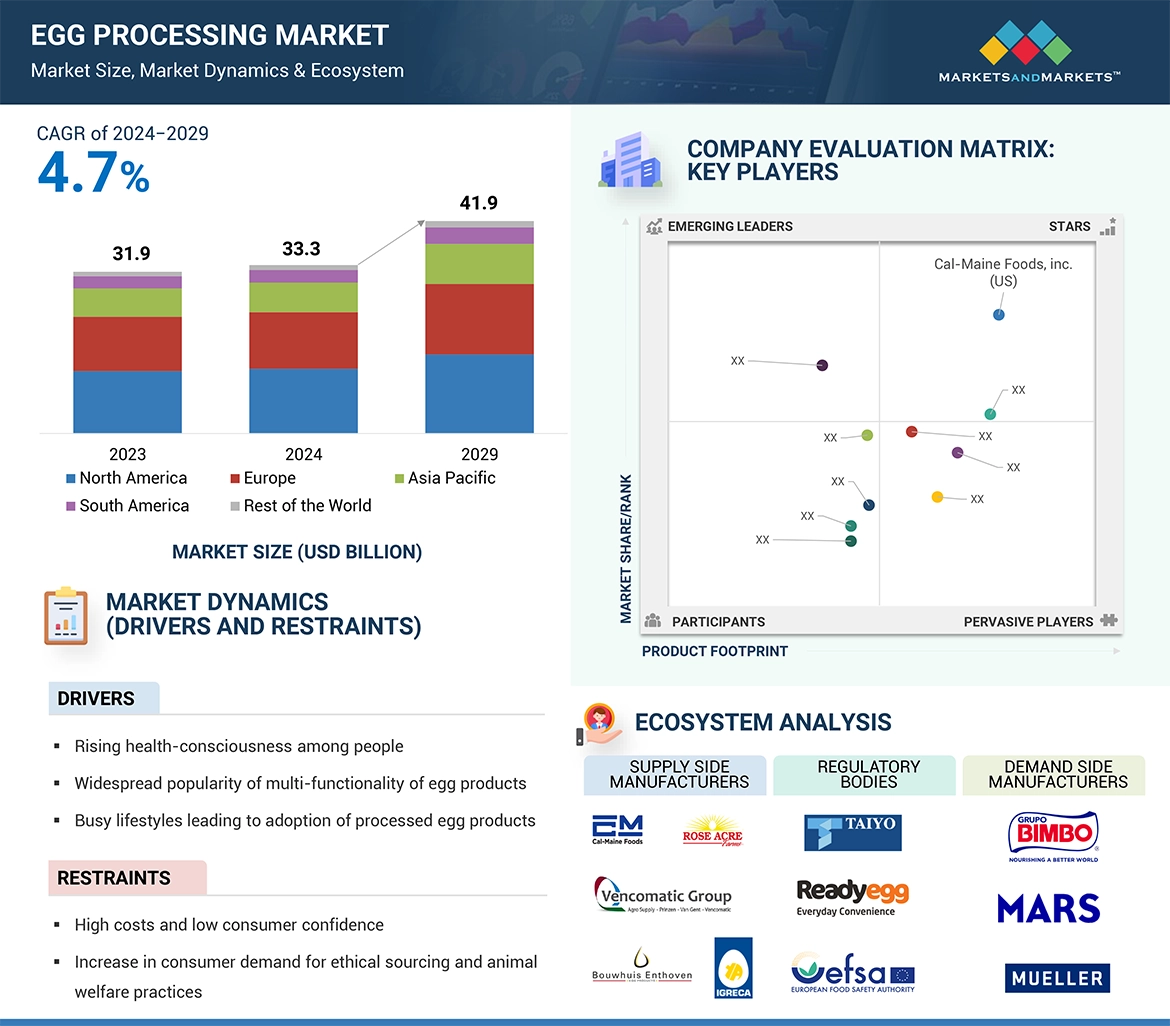

In response to these shifting preferences, leading producers like Cal-Maine Foods and Rose Acre Farms have been investing heavily in cage-free production systems. Cal-Maine Foods, one of the largest egg producers in the U.S., is expanding its cage-free operations to meet growing demand for ethically sourced eggs. Similarly, Rose Acre Farms has committed to transitioning all its hens to cage-free housing by 2026, emphasizing their dedication to animal welfare and ethical sourcing.

The egg processing industry continues to evolve, driven by trends such as rising demand for cage-free and organic eggs, advancements in processing technologies that improve product quality, and growing focus on sustainability and traceability. Technology adoption aimed at boosting operational efficiency also plays a critical role. Staying informed about these developments is essential for stakeholders to capitalize on new opportunities and navigate the dynamic landscape of the egg processing market.

Egg Processing Market Growth Drivers

- Rising Demand for Convenience Foods: Busy lifestyles and urbanization have led consumers to seek quick and easy meal solutions. Processed egg products such as liquid eggs and powdered eggs offer convenience for food manufacturers and restaurants, speeding up preparation times.

- Health and Nutrition Awareness: Eggs are a rich source of high-quality protein, vitamins, and minerals. Processed egg products enable easier integration into various health-oriented food products such as protein bars, supplements, and infant nutrition formulas.

- Expansion of Foodservice Industry: The global growth of cafes, bakeries, fast food chains, and catering services drives demand for consistent, safe, and easy-to-use egg products.

- Technological Advancements: Improvements in egg pasteurization, drying, and packaging technologies have enhanced the safety, shelf life, and quality of processed egg products, making them more appealing to consumers and manufacturers alike.

The organic egg products segment is poised for rapid growth over the coming years.

Rising consumer demand for organic egg products is fueled by increasing awareness around health benefits, food safety, animal welfare, and environmental sustainability. Data from the United Egg Producers highlights this trend: Organic and cage-free shell egg production climbed from 29.3% (96.1 million hens) in 2021 to 34% (106.2 million hens) in 2022. This growth reflects consumers’ growing concerns about the humane treatment of food animals. Organic certification standards ensure hens have outdoor access and are raised without antibiotics or growth hormones, appealing to ethically minded buyers.

Insights from the Egg Carton Store Blog (September 2023) further underscore the surge in organic egg product demand, driven by health-conscious shoppers seeking premium, ethically produced food. Many consumers are willing to pay a premium for organic eggs due to their perceived superior quality and sustainable production methods. Factors such as rising disposable incomes, wider product availability, and strategic marketing efforts are amplifying this growth. For example, EIPRO-Vermarktung GmbH & Co. KG (Germany) offers a broad portfolio of organic egg products—including whole eggs, yolks, whites, as well as liquid and frozen egg alternatives—all pasteurized for safety and available in various packaging formats.

Asia Pacific Dominates the Egg Processing Market Share.

The Asia Pacific (APAC) egg processing market includes key countries such as Japan, China, India, Australia, New Zealand, and others in the region. According to a 2023 article by WATT Poultry, the outlook for Asia’s poultry and egg producers remains optimistic. This positive trajectory is supported by rising incomes, rapid urbanization, enhanced disease control measures, and the integration of advanced technologies, which collectively create favorable long-term conditions for growth.

Nevertheless, the sector faces ongoing challenges like price volatility, stricter animal welfare regulations, and mounting pressure to adopt sustainable practices amid growing environmental concerns. Persistent disease threats also demand continued innovation and investment in biosecurity to protect poultry health and maintain market stability. These multifaceted issues highlight the importance of strategic planning and cross-industry collaboration within the APAC poultry and egg sectors.

Leading Egg Processing Companies:

Prominent industry players, including Cal-Maine Foods, Inc. (US), Rose Acre Farms (US), Ovobel Foods Limited (India), SKMEgg.com (India), Interovo Egg Group BV (Netherlands), IGRECA (France), Eurovo Srl (Italy), Avril SCA (France), Rembrandt Foods (US), and Hillandale Farms (US), wield substantial influence in the egg processing market. These entities boast robust manufacturing facilities and well-established distribution networks across pivotal regions such as North America, Europe, South America, and the Asia Pacific, ensuring a widespread presence and accessibility of their products.

Future Outlook

The egg processing market is poised for innovation and growth, driven by continued demand for protein-rich and convenient foods. Key trends to watch include:

- Development of organic and specialty egg products catering to health-conscious consumers.

- Adoption of clean-label and allergen-free processed eggs.

- Increased use of automation and AI in egg processing plants for improved efficiency.

- Expansion of processed egg applications in nutraceuticals and cosmetics.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=124810046

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s Best Management Consulting Firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. With the widest lens on emerging technologies, we are proficient in co-creating supernormal growth for clients across the globe.

Today, 80% of Fortune 2000 companies rely on MarketsandMarkets, and 90 of the top 100 companies in each sector trust us to accelerate their revenue growth. With a global clientele of over 13,000 organizations, we help businesses thrive in a disruptive ecosystem.

The B2B economy is witnessing the emergence of $25 trillion in new revenue streams that are replacing existing ones within this decade. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines – TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ‘GIVE Growth’ principle, we collaborate with several Forbes Global 2000 B2B companies to keep them future-ready. Our insights and strategies are powered by industry experts, cutting-edge AI, and our Market Intelligence Cloud, KnowledgeStore™, which integrates research and provides ecosystem-wide visibility into revenue shifts.

Media Contact

Company Name: MarketsandMarkets™ Research Private Ltd.

Contact Person: Mr. Rohan Salgarkar

Email: Send Email

Phone: 18886006441

Address:1615 South Congress Ave. Suite 103, Delray Beach, FL 33445

City: Florida

State: Florida

Country: United States

Website: https://www.marketsandmarkets.com/Market-Reports/egg-processing-equipment-market-124810046.html

Press Release Distributed by ABNewswire.com

To view the original version on ABNewswire visit: Egg Processing Market Trends, Growth Drivers, Key Segments, and Future Outlook