The Managed Application Services Market is experiencing substantial growth due to the increasing reliance of businesses on cloud-based applications and IT infrastructure management. Managed application services involve outsourcing the maintenance, support, and monitoring of enterprise applications to specialized service providers, ensuring optimal performance, security, and compliance. This market is driven by the need for businesses to reduce operational costs, enhance efficiency, and focus on core competencies while leaving application management to experts. The demand for managed application services is fueled by digital transformation initiatives across industries, the rapid adoption of Software-as-a-Service (SaaS) solutions, and the increasing complexity of enterprise applications. Additionally, businesses are embracing managed services to address cybersecurity concerns, ensure regulatory compliance, and enhance the scalability of their IT infrastructure. The growing trend of remote work and the need for seamless application performance across multiple locations further contribute to market expansion. Organizations across diverse sectors, including healthcare, BFSI, IT and telecommunications, manufacturing, and retail, are integrating managed application services to streamline operations and improve overall productivity.

Get An Exclusive Sample of the Research Report at: https://www.marketresearchfuture.com/sample_request/24262

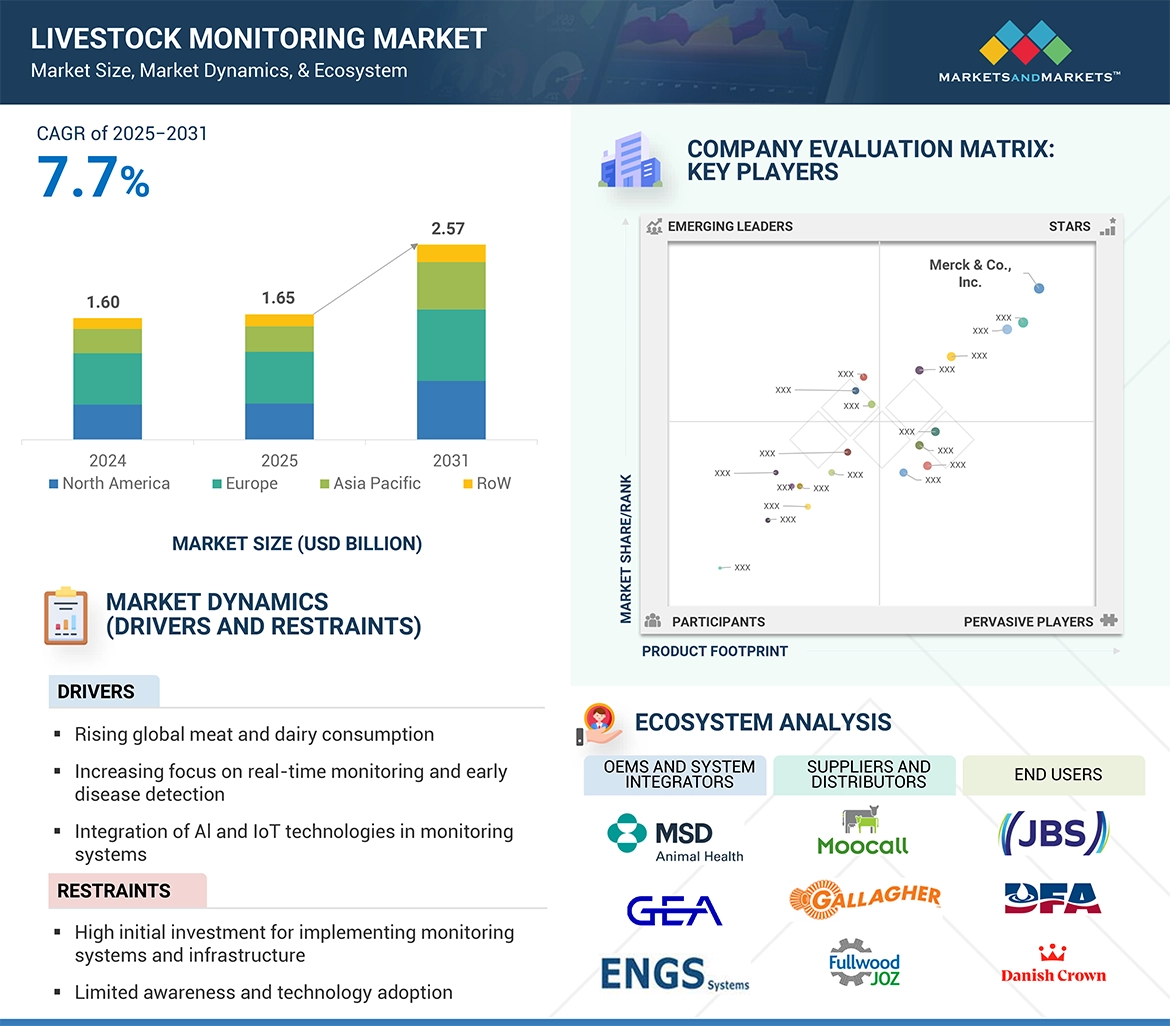

Market Segmentation

The Managed Application Services Market can be segmented based on service type, deployment model, organization size, and industry vertical. Service types include application monitoring, application security, hosting services, database management, and disaster recovery services. Deployment models are categorized into on-premises and cloud-based solutions, with cloud-based services gaining significant traction due to their cost-effectiveness, scalability, and ease of access. Small and medium-sized enterprises (SMEs) are increasingly adopting managed application services alongside large enterprises to ensure robust application performance without the need for extensive in-house IT teams. Industry verticals utilizing managed application services range from banking, financial services, and insurance (BFSI) to healthcare, IT and telecom, retail, manufacturing, and government organizations. The adoption of managed application services is particularly strong in industries that require high levels of security, compliance, and real-time application monitoring, such as finance and healthcare.

Market Key Players

The Managed Application Services Market is highly competitive, with several key players driving innovation and service delivery. Leading companies in this market include:

- HCL Technologies

- Accenture

- Wipro

- Cognizant

- TCS

- IBM

- Atos

- NTT DATANewparaDXC Technology

- Computer Sciences Corporation

- Capgemini

- HP Enterprises

- Microsoft

- DXC Technology

- Infosys

Market Opportunities

The increasing adoption of cloud computing and hybrid IT environments presents significant growth opportunities for the Managed Application Services Market. Organizations are leveraging managed services to navigate the complexities of multi-cloud environments, ensuring seamless integration and performance optimization. The rise of AI and automation in application management is another major opportunity, enabling predictive maintenance, proactive security measures, and self-healing applications. Additionally, the growing importance of cybersecurity and compliance in highly regulated industries provides opportunities for service providers to offer specialized security and risk management solutions. With the expanding adoption of digital transformation initiatives, there is a growing demand for industry-specific managed services tailored to the unique needs of different sectors, such as healthcare, finance, and manufacturing. Emerging markets in Asia-Pacific, Latin America, and the Middle East are also providing lucrative opportunities as businesses in these regions invest in advanced IT infrastructure and cloud-based applications.

Restraints and Challenges

Despite its promising growth, the Managed Application Services Market faces several challenges and restraints. One of the primary challenges is data security and privacy concerns, as businesses entrust third-party service providers with sensitive information and critical applications. Ensuring compliance with data protection regulations, such as GDPR, HIPAA, and PCI DSS, remains a significant challenge for service providers. Additionally, integration complexities with legacy IT systems pose a barrier to adoption, especially for large enterprises with established infrastructure. High initial investment costs for managed services can also be a deterrent for SMEs, limiting market penetration in this segment. Moreover, the shortage of skilled IT professionals with expertise in cloud management, cybersecurity, and AI-driven automation presents a challenge for service providers looking to scale their offerings. The evolving threat landscape, including sophisticated cyberattacks and ransomware incidents, further complicates managed application security and requires continuous investment in threat detection and mitigation strategies.

Regional Analysis

The Managed Application Services Market exhibits significant regional variations in adoption and growth rates. North America dominates the market, driven by the presence of established IT infrastructure, a high concentration of enterprises, and strong investments in cloud computing and digital transformation initiatives. The United States is a key contributor to market growth, with major technology companies and service providers driving innovation and service expansion. Europe follows closely, with countries such as the United Kingdom, Germany, and France leading in managed application service adoption due to stringent regulatory compliance requirements and the need for robust cybersecurity solutions. The Asia-Pacific region is experiencing rapid growth in this market, fueled by increasing cloud adoption, expanding IT infrastructure, and government initiatives promoting digitalization. Countries such as China, India, and Japan are witnessing a surge in demand for managed services, particularly among SMEs looking for cost-effective IT management solutions. Latin America and the Middle East & Africa are emerging markets with growing adoption, driven by investments in digital infrastructure and the rising need for application performance optimization in various industries.

Recent Developments

The Managed Application Services Market is witnessing continuous advancements driven by technology innovations, strategic partnerships, and service expansions. Leading market players are incorporating AI, automation, and machine learning into their service offerings to enhance application monitoring, predictive maintenance, and security. Several companies are investing in hybrid cloud solutions to address the growing demand for seamless integration between on-premises and cloud-based applications. The industry is also seeing increased collaboration between managed service providers and cloud computing giants such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud to offer comprehensive cloud-based application management solutions. Furthermore, cybersecurity enhancements remain a top priority, with service providers integrating advanced threat detection, endpoint protection, and compliance management tools into their managed services portfolios. The rise of remote work has also prompted businesses to invest in managed application services that ensure secure and efficient application performance across distributed workforces. As the market evolves, continued investments in innovation, talent acquisition, and global expansion will shape the future trajectory of the Managed Application Services Market.

Check Out More Related Insights:

Customer Engagement Hub Market –https://www.marketresearchfuture.com/reports/customer-engagement-hub-market-24115

About Market Research Future:

At Market Research Future (MRFR), we enable our customers to unravel the complexity of various industries through our Cooked Research Report (CRR), Half-Cooked Research Reports (HCRR), Raw Research Reports (3R), Continuous-Feed Research (CFR), and Market Research & Consulting Services.

MRFR team have supreme objective to provide the optimum quality market research and intelligence services to our clients. Our market research studies by products, services, technologies, applications, end users, and market players for global, regional, and country level market segments, enable our clients to see more, know more, and do more, which help to answer all their most important questions.

Media Contact

Company Name: Market Research Future

Contact Person: Media Relations

Email: Send Email

Country: United States

Website: https://www.marketresearchfuture.com

Press Release Distributed by ABNewswire.com

To view the original version on ABNewswire visit: Managed Application Services Market Expands Rapidly: Projected CAGR of 12.72% Through 2034