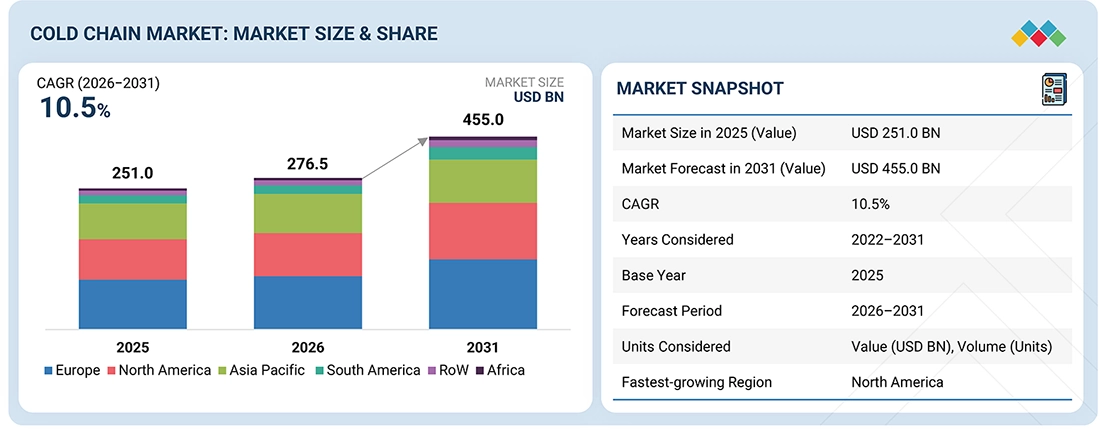

According to a research report published by MarketsandMarkets™, The cold chain market is estimated at USD 276.5 billion in 2026 and is projected to reach USD 455.0 billion by 2031, at a CAGR of 10.5% from 2026 to 2031. Temperature-controlled logistics are gaining more and more prominence in many industries; hence, the market is experiencing substantial growth. In the healthcare industry, it is critical that medications and vaccines undergo proper temperature control so that they remain safe and effective. With an increase in the number of drugs that are more vulnerable to temperature, there is a need for adequate cold chain capabilities.

In the food and beverage industry, the cold chain process is necessary in preserving fresh goods and increasing shelf life, thus ensuring minimal losses of perishable foods such as dairy products, meat, seafood, fruits, vegetables, juices, and other beverages. The chemical industry also needs cold chains since many chemicals and raw materials require temperature control for their safety and effectiveness.

Besides this, there are a number of other uses of cold chain logistics. Temperature-controlled environments are also vital when it comes to the storage and transportation of important pieces of artwork, as well as historical relics. Extreme temperatures may harm the functioning of certain electronic devices. Flowers and plants, too, need temperature-controlled logistics to maintain their freshness. Consequently, cold chains have become necessary in order to maintain product quality and safety in many different industries.

Market Size and Growth Forecast

- Market Size in 2025 (Value): USD 251.0 Billion

- Market Forecast in 2030 (Value): USD 455.0 Billion

- Growth Rate: CAGR of 10.5% during 2026-2031

- Years Considered: 2022–2031

- Base Year: 2025

- Forecast Period: 2026–2031

- Units Considered: Value (USD Billion), Volume (Units)

- Report Coverage: Revenue forecast, company ranking, competitive landscape, growth factors, and trends

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=811

By type, the cold chain storage & infrastructure segment accounts for a significant market share.

Cold chain storage & infrastructure is one of the largest segments within the cold chain market, owing to the rising requirement for temperature-controlled warehousing and logistics for different industries like food & beverages, pharma, and chemicals. Increased consumption of perishable goods, growth in organized retailing and online grocery delivery, along with increased requirements in pharmaceuticals, have led to investment in refrigerated storage solutions and monitoring systems. Growth in international trade in temperature-controlled goods has added to the demand for cold chain solutions, ensuring that products do not spoil.

Developments in technology related to the cold chain infrastructure include IoT-based temperature monitoring equipment, automated refrigerators, and energy-efficient storage facilities, and all of these are contributing towards the growth of this segment. Governmental as well as private sector initiatives for developing modern cold storage facilities are aimed at improving food security levels, minimizing post-harvest losses, and ensuring compliance with regulations regarding pharmaceutical/biological materials. The adoption of cold chain logistics across emerging nations will continue to drive the expansion of this segment going forward.

By refrigerated road transportation type, the refrigerated LCV segment is estimated to maintain strong growth.

The versatility and agility of refrigerated LCVs make them ideal for navigating through urban areas and reaching smaller distribution points, thereby offering enhanced accessibility to a wider range of customers. Additionally, the lower operational costs associated with LCVs, including fuel consumption and maintenance expenses, render them more economically viable for businesses operating within the cold chain sector. Moreover, the increasing emphasis on sustainability and environmental concerns has prompted a shift towards smaller, more fuel-efficient vehicles like LCVs, aligning with the industry’s efforts to reduce carbon emissions and minimize ecological impact.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=811

Based on region, Europe accounts for a significant market share.

The region holds a considerable share in the global cold chain market owing to high demand for temperature management solutions within food and beverages, pharmaceutical, and healthcare sectors. The presence of stringent laws governing food security, transportation of pharmaceutical products, and product quality has led to the widespread use of advanced refrigeration technology. The regulatory policies implemented by the European Union help to build cold chains in an effective manner that helps to save food waste and ensure product integrity.

Nations like Germany, France, the UK, Italy, and the Nordic countries continue to experience constant investments in their cold storage facilities and refrigeration warehousing services. The continent has good transport and logistical infrastructure, which, coupled with the adoption of modern digital technology such as the Internet of Things (IoT), enhances its attractiveness for cold chain logistics. Moreover, the rising demand for frozen foods, biologics, vaccines, and fresh produce continues to make Europe an important player in the international cold chain logistics market.

Leading Cold Chain Companies:

The report profiles key playerssuch as Americold Logistics, Inc. (US), Lineage, Inc. (US), NICHIREI CORPORATION (Japan), Burris Logistics (US), A.P. Moller – Maersk (Denmark), Tippmann Group (US), Coldman Logistics Pvt. Ltd. (India), and United States Cold Storage (US).

Recent Developments in the Cold Chain Industry:

- May 2026: Americold expanded its partnership with PLUS, a Dutch supermarket cooperative with around 440 stores, to centralize frozen logistics operations across the Netherlands. Through its Barneveld distribution center, Americold will manage storage, handling, and distribution of frozen products, helping PLUS improve supply chain efficiency, service quality, and nationwide logistics integration.

- April 2026: The Nichirei Logistics Group acquired two cold chain companies based in Indonesia, namely PT Mega Indo Logistik and PT Mega Internasional Sejahtera, as consolidated subsidiaries. This acquisition is in keeping with the company’s efforts to develop its temperature-controlled logistics network within ASEAN as well as to enhance overseas expansion in Indonesia’s booming cold chain industry.

- April 2025: Lineage, Inc. is planning on adding more cold storages within the United States through acquisitions, greenfield development, and automation. In connection with its strategic vision, the firm has entered into a deal to purchase several cold storage units from Tyson Foods. This would help reinforce the long-term relationship that has been built between Lineage and Tyson. Lineage will be building and operating two highly automated cold storage facilities, with Tyson Foods being the key customer of these operations.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=811

About MarketsandMarkets™

MarketsandMarkets™ has been recognized as one of America’s Best Management Consulting Firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. With the widest lens on emerging technologies, we are proficient in co-creating supernormal growth for clients across the globe.

Today, 80% of Fortune 2000 companies rely on MarketsandMarkets, and 90 of the top 100 companies in each sector trust us to accelerate their revenue growth. With a global clientele of over 13,000 organizations, we help businesses thrive in a disruptive ecosystem.

The B2B economy is witnessing the emergence of $25 trillion in new revenue streams that are replacing existing ones within this decade. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines – TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ‘GIVE Growth’ principle, we collaborate with several Forbes Global 2000 B2B companies to keep them future-ready. Our insights and strategies are powered by industry experts, cutting-edge AI, and our Market Intelligence Cloud, KnowledgeStore™, which integrates research and provides ecosystem-wide visibility into revenue shifts.

Media Contact

Company Name: MarketsandMarkets™ Research Private Ltd.

Contact Person: Mr. Rohan Salgarkar

Email: Send Email

Phone: 18886006441

Address:1615 South Congress Ave. Suite 103, Delray Beach, FL 33445

City: Florida

State: https://www.marketsandmarkets.com/Market-Reports/cold-chain-market-811.html

Country: United States

Website: https://www.marketsandmarkets.com/Market-Reports/cold-chain-market-811.html

Press Release Distributed by ABNewswire.com

To view the original version on ABNewswire visit: Cold Chain Market to Reach $455.0 Billion by 2031, Growing at a CAGR of 10.5% – Exclusive Report by MarketsandMarkets™