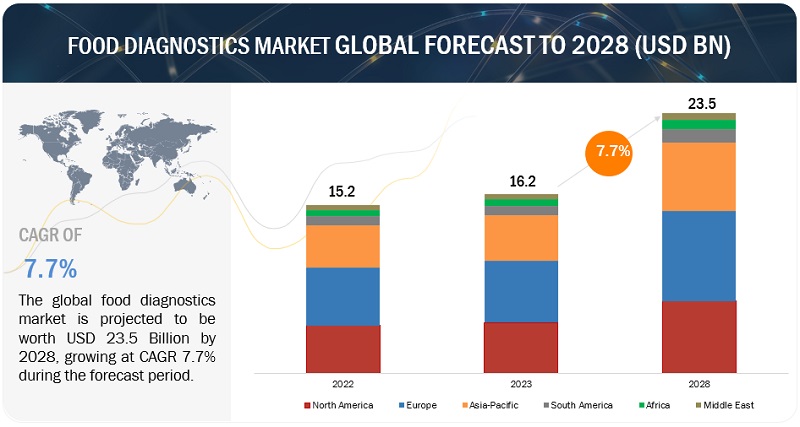

The food diagnostics market size is valued at USD 16.2 billion in 2023 and is expected to grow to USD 23.5 billion by 2028, with a CAGR of 7.7% during this period. Food diagnostics refers to the set of processes and techniques used to assess and validate food products, ensuring they meet safety, quality, authenticity, and regulatory standards. These procedures include various testing methods and analytical tools applied throughout the food supply chain, from production and processing to distribution and consumption. They play a critical role in maintaining and evaluating key quality attributes such as taste, texture, color, aroma, and overall sensory properties of food products.

Global Food Diagnostics Market Drivers:

The surge in food recalls has significantly driven the growth of the food diagnostics industry, fueled by heightened concerns over food safety and public health. Contaminated or unsafe food products can lead to serious consequences, including illnesses, hospitalizations, and even fatalities. This increased focus on food safety has encouraged regulatory authorities and food manufacturers to invest in advanced diagnostic technologies. These solutions provide rapid and accurate detection of contaminants, pathogens, allergens, and adulterants, helping prevent tainted products from reaching consumers. Additionally, the financial and reputational risks associated with recalls have pushed companies to adopt state-of-the-art diagnostic tools, contributing to the expansion of the food diagnostics market.

Food Diagnostics Market Trends

Here are some of the key trends currently shaping the Food Diagnostics Market:

Increased Focus on Food Safety and Quality Control: Rising consumer demand for safe and high-quality food products is driving the adoption of advanced diagnostics technologies to detect contaminants, pathogens, and toxins across the food supply chain.

Growth of Rapid Diagnostic Technologies: Rapid testing solutions, such as PCR-based tests, biosensors, and immunoassays, are gaining traction as they offer faster and more accurate results, reducing the time between sample collection and analysis.

Automation and AI Integration: Automation in food testing labs, coupled with AI and machine learning algorithms, is enhancing the efficiency, speed, and precision of food diagnostics, particularly for large-scale operations.

Rising Need for Allergen Testing: With food allergies becoming more prevalent, the demand for testing products that can detect allergens in processed and packaged foods is increasing, encouraging innovation in this niche.

Growth in Non-Destructive Testing Methods: Non-invasive and non-destructive diagnostic methods, such as spectroscopy and imaging technologies, are becoming more common to ensure food quality without damaging the products.

Stringent Regulatory Frameworks: Governments and regulatory bodies are imposing stricter standards for food safety, which is pushing food manufacturers to adopt more rigorous diagnostics systems to comply with these regulations.

Focus on Sustainable Food Production: As sustainability becomes a priority in the food industry, there is an increased focus on testing methods that are environmentally friendly, using fewer chemicals and generating less waste.

Emergence of Blockchain for Food Traceability: Blockchain technology is being integrated with food diagnostics systems to enhance transparency, traceability, and data integrity in the food supply chain, ensuring that any contamination is easily traceable.

Food Diagnostics Market Opportunities: Increased budget allocation and expenditure on food safety

Governments, regulatory bodies, and key players in the food industry around the world are increasingly recognizing the critical importance of safeguarding the food supply chain. This heightened awareness has spurred a significant rise in investments in food safety initiatives, driving innovation and expansion within the food diagnostics market. The adoption of cutting-edge technologies, such as DNA-based testing and rapid pathogen detection, is accelerating, providing more accurate and efficient food monitoring from production to consumption. Additionally, growing consumer awareness of foodborne diseases and the increasing demand for transparency in the supply chain have amplified the need for comprehensive diagnostic solutions. As a result, the evolving landscape offers substantial opportunities for companies to create advanced diagnostic tools and services, positioning the food diagnostics market for considerable growth and improved food safety.

Asia Pacific Projected to Lead Global Food Diagnostics Market Growth with Highest CAGR

The Asia Pacific region is undergoing notable population growth, urbanization, and a rise in disposable income. Countries such as China and India are experiencing rapid population increases, which has led to higher food consumption. This surge in demand underscores the critical need for effective food safety and quality testing. As more individuals move to urban areas, there is a growing demand for processed and packaged foods. This escalating demand necessitates rigorous quality control and safety measures, thereby propelling the growth of the food diagnostics market.

Additionally, the food supply chain in the Asia Pacific is becoming more intricate due to globalization and the expansion of international trade. This complexity requires thorough testing and monitoring throughout the entire supply chain, from farm to table. Consequently, food diagnostics solutions are increasingly vital for ensuring the safety and quality of food products.

Top Food Diagnostics Companies:

Bio-Rad Laboratories Inc. (US), Thermo Fisher Scientific Inc. (US), Shimadzu Corporation (Japan), Neogen Corporation (US), BioMerieux (France), Agilent Technologies Inc. (US), Merck KGaA (Germany), QIAGEN (Germany), Bruker (US), and Danaher (US) are among the key players in the global food diagnostics market. To increase their company’s revenues and market shares, companies are focusing on launching new products, developing partnerships, and acquiring other companies. The key strategies used by companies in the food diagnostics market include geographical expansion to tap the potential of emerging economies, strategic acquisitions to gain a foothold over the extensive supply chain, and new product launches as a result of extensive research and development (R&D) initiatives.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=225194671

Key Questions Addressed by the Food Diagnostics Market Report:

What is the food diagnostics market?

Why is food diagnostics important?

Which segment by food tested accounted for the largest food diagnostics market share?

What are the major drivers of the food diagnostics market?

What are the challenges faced by the food diagnostics market?

Who are the key players in the food diagnostics market?

What are the emerging trends in the food diagnostics market?

How is the food diagnostics market expected to grow in the coming years?

What is the future outlook for the food diagnostics market?

Which region is projected to account for the largest share of the food diagnostics market?

What is the current size of the global food diagnostics market?

Schedule a call with our Analysts to discuss your business needs: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=225194671

About MarketsandMarkets™

MarketsandMarketsTM has been recognized as one of America’s best management consulting firms by Forbes, as per their recent report.

MarketsandMarkets™ is a blue ocean alternative in growth consulting and program management, leveraging a man-machine offering to drive supernormal growth for progressive organizations in the B2B space. We have the widest lens on emerging technologies, making us proficient in co-creating supernormal growth for clients.

Earlier this year, we made a formal transformation into one of America’s best management consulting firms as per a survey conducted by Forbes.

The B2B economy is witnessing the emergence of $25 trillion of new revenue streams that are substituting existing revenue streams in this decade alone. We work with clients on growth programs, helping them monetize this $25 trillion opportunity through our service lines – TAM Expansion, Go-to-Market (GTM) Strategy to Execution, Market Share Gain, Account Enablement, and Thought Leadership Marketing.

Built on the ‘GIVE Growth’ principle, we work with several Forbes Global 2000 B2B companies – helping them stay relevant in a disruptive ecosystem. Our insights and strategies are molded by our industry experts, cutting-edge AI-powered Market Intelligence Cloud, and years of research. The KnowledgeStore™ (our Market Intelligence Cloud) integrates our research, facilitates an analysis of interconnections through a set of applications, helping clients look at the entire ecosystem and understand the revenue shifts happening in their industry.

Media Contact

Company Name: MarketsandMarkets™ Research Private Ltd.

Contact Person: Mr. Rohan Salgarkar

Email: Send Email

Phone: 18886006441

Address:1615 South Congress Ave. Suite 103

City: Delray Beach

State: FL 33445

Country: United States

Website: https://www.marketsandmarkets.com/Market-Reports/food-diagnostics-systems-225194671.html

Press Release Distributed by ABNewswire.com

To view the original version on ABNewswire visit: Food Diagnostics Market Overview, Growth Drivers, Key Segments, Latest Trends, Regional Insight, Recent Developments, and Top Companies